How the ₪2.90 Shekel Is Crushing American Buyers in Israel’s Housing Market

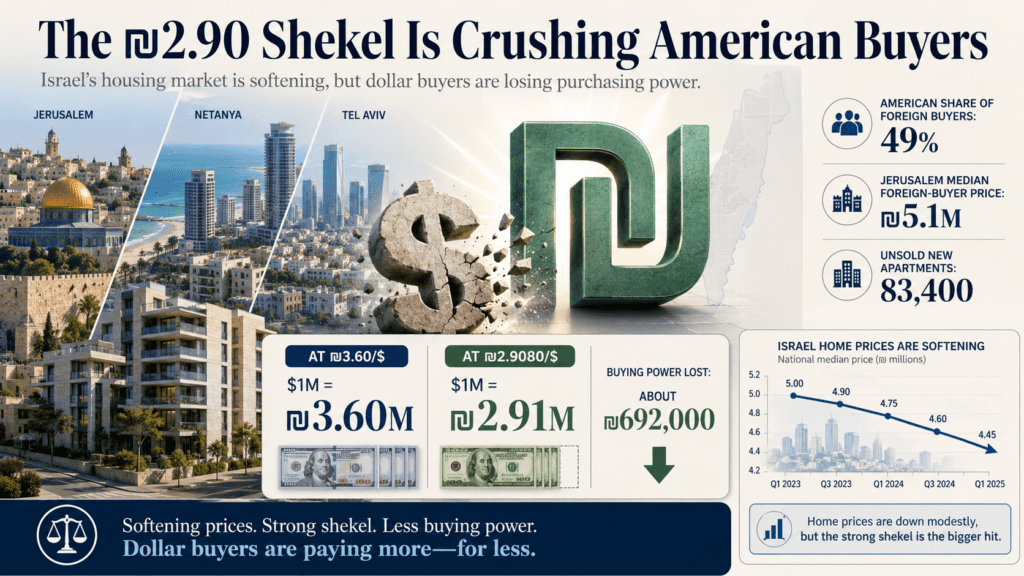

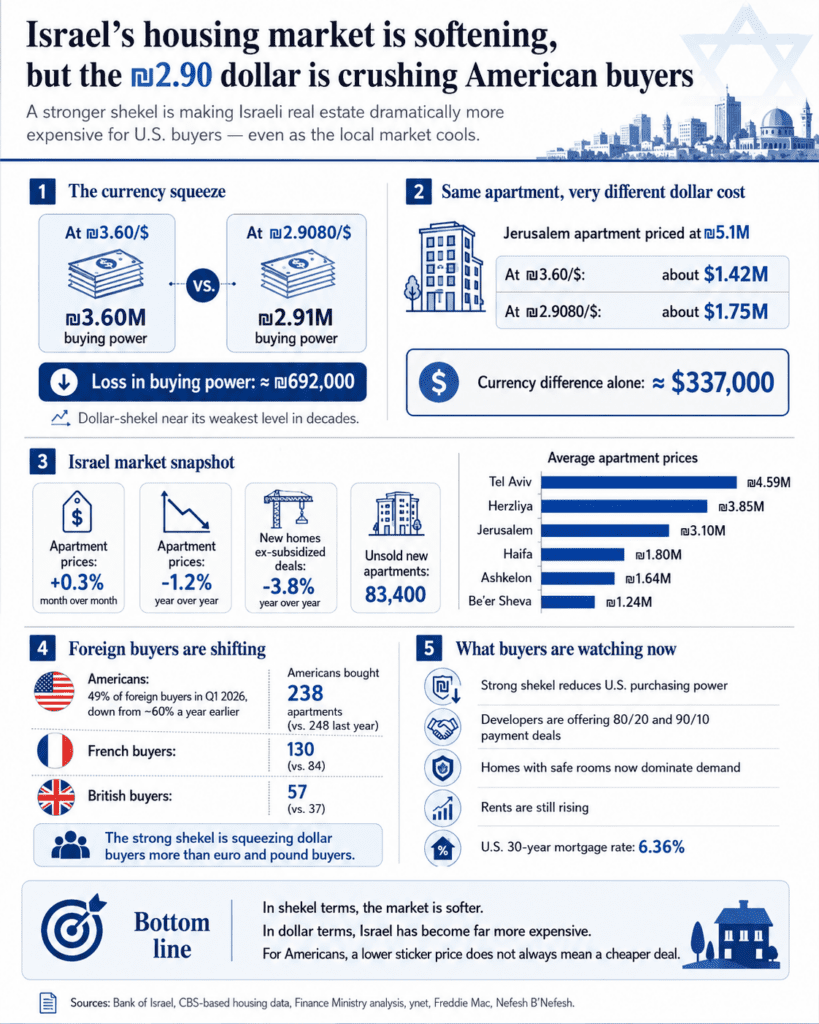

The shekel is trading around ₪2.90 to the dollar, the lowest level since 1993. For an American family trying to buy in Jerusalem, Netanya, Beit Shemesh or Tel Aviv, this is major. A $1 million budget at ₪3.60 bought ₪3.6 million. At ₪2.90, it buys about ₪2.91 million. That is a loss of roughly ₪692,000 in buying power before the buyer even negotiates, hires a lawyer, pays tax or speaks to a mortgage broker.

That is what makes the Israeli housing market so strange right now. On paper, buyers finally have leverage. The latest CBS-based housing data showed apartment prices rising 0.3% month over month, but still down 1.2% year over year. New apartment prices rose slightly, but excluding subsidized government deals, new-home prices actually fell, and were down 3.8% annually. The national average apartment price stood around ₪2.33 million, while Tel Aviv averaged ₪4.59 million, Herzliya ₪3.85 million, Jerusalem ₪3.1 million, Be’er Sheva ₪1.24 million, Ashkelon ₪1.64 million and Haifa ₪1.8 million.

For dollar buyers, though, a modest Israeli price drop can be wiped out instantly by the exchange rate. A Jerusalem apartment priced at ₪5.1 million costs about $1.75 million at today’s Bank of Israel rate. At ₪3.60 to the dollar, that same apartment would have cost about $1.42 million. Same apartment. Same street. Same seller. A roughly $337,000 difference created by currency alone.

That explains why the American buyer story has changed. A new Finance Ministry analysis found that American passport holders still made up the largest group of foreign buyers in Israel, but their share fell to 49% of foreign purchases in the first quarter, down from about 60% a year earlier. Americans bought 238 apartments, slightly below the 248 they bought in the same period last year, while French purchases jumped from 84 to 130 and British purchases rose from 37 to 57. Government economists directly pointed to the dollar’s 13.6% depreciation against the shekel, compared with a much smaller 4% decline for the euro.

The American map is also revealing. More than half of American purchases were in Jerusalem, where the median foreign-buyer purchase price hit ₪5.1 million. About 60% of the apartments Americans bought in Jerusalem were new homes, with a median price of ₪5.95 million. Netanya overtook Beit Shemesh as the second-most active American-buyer market, while Tel Aviv ranked only fifth among Americans, behind Kiryat Gat.

That matters because this is not a broad “foreigners stopped buying Israel” story. It is more specific. Dollar-based buyers are being squeezed. Euro and pound buyers are seeing a different calculation. French buyers, for example, are buying more modestly priced homes, with an average purchase price of ₪2.8 million, and are spreading into Netanya, Jerusalem, Tel Aviv and Bat Yam. Americans are still buying, but they are concentrated in expensive markets where every currency move is amplified.

The shekel’s strength is not happening in a vacuum. The Bank of Israel says the shekel strengthened against the dollar, the euro and Israel’s broader trading partners in the first quarter, even as volatility rose during Operation Roaring Lion against Iran. Reuters reported that the shekel has been supported by a weaker global dollar, rising Israeli equities and large foreign investment into Israel. Bank of Israel Deputy Governor Andrew Abir said the central bank is not rushing to intervene, even while acknowledging that markets may be over-optimistic.

That creates a sharp divide. For Israelis earning shekels, the strong currency helps tame import prices and inflation. For exporters and foreign buyers, it hurts. For American Jews who kept money in dollars while planning an eventual Israel purchase, it can feel like the market moved against them even when apartment prices did not.

The irony is that this should be one of the better negotiating environments Israel has offered in years. Developers are sitting on heavy inventory. Ynet, citing Bank of Israel data, reported that contractors held a record 83,400 unsold new apartments at the end of 2025, while apartment purchases fell 12% from the previous year. The same report said 44% of projects financed by Israel’s five largest banks had construction progressing faster than sales, a sign of pressure beneath the surface.

That pressure is visible in the sales tactics. The 80/20 and 90/10 deals that became common in Israel let buyers pay only 10% or 20% upfront and the balance near delivery. Those offers helped developers keep sales moving during the slowdown, but they also created risk: some buyers may now struggle to close, especially if their dollars are worth less, their U.S. home sale is delayed, or their mortgage terms change before delivery.

Still, Israel is not a crash market. It is a compressed market. The country has too many unsold apartments in some places and not enough of the right apartments in others. A Shoresh Institution study cited by The Jerusalem Post found that from 1990 to 2023, household growth outpaced construction starts by about 121,000 apartments, and the gap reached about 272,000 when measured against completed apartments. The deeper problem is not just quantity, but mismatch: Israel keeps building large four- and five-room apartments while more Israelis live in smaller households and need smaller, more affordable units.

Rent tells the same story. Even as purchase prices soften, rents keep rising. Recent data showed rents up 2.6% for tenants renewing leases and 3.6% for new tenants, while residential construction input costs rose 3% over the year, driven partly by a 4.7% increase in labor costs. That combination makes sellers stubborn: if they can rent, wait and avoid cutting too deeply, many will.

Security has also changed the buyer checklist. In March, homes with safe rooms accounted for 65% of secondhand transactions, the highest level recorded since at least early 2024. Investor sales fell sharply, especially in Tel Aviv and Haifa, where many older apartments lack safe rooms. The message is clear: buyers are not only comparing price, view and neighborhood anymore. A mamad can now affect liquidity, resale value and family decision-making.

For Americans, the pressure is doubled by the U.S. side of the equation. Freddie Mac reported the average 30-year fixed mortgage rate at 6.36%, while Reuters said the U.S. housing market remains weighed down by elevated borrowing costs, tight entry-level inventory and high home prices. That matters because many Israel buyers do not arrive with idle cash sitting in a shekel account. They are selling a U.S. home, borrowing against assets, liquidating investments or timing a transfer. A slow U.S. sale plus a strong shekel can turn a planned Israel purchase into a moving target.

Tax status can make the gap even wider. Foreign residents are generally treated like Israeli investors for purchase tax, with rates of 8% up to ₪6,055,070 and 10% above that level. Israeli residents buying a sole residence start at lower brackets, and qualifying olim can receive special purchase-tax benefits under updated rules. For an American buyer on a multimillion-shekel purchase, tax planning is not a side issue. It can be a six-figure shekel decision.

So what does this market actually mean?

It does not mean Americans should panic-buy because the shekel is strong. It also does not mean waiting automatically solves the problem. If the dollar rebounds, a buyer who waited may suddenly regain hundreds of thousands of shekels in purchasing power. If the shekel stays strong and Israeli rates fall, local buyers may return, developers may regain confidence and today’s negotiating window may narrow.

The smarter read is that Israeli real estate has split into two markets. In shekel terms, buyers can find softness, especially in parts of the new-build market and in areas where developers need cash flow. In dollar terms, Israel has become dramatically more expensive. That is why some Americans are pausing, some are lowering budgets, some are shifting from Jerusalem to Netanya or Beit Shemesh, and some are deciding that if they are buying Israel for life rather than speculation, the currency pain is the price of certainty.

The best-positioned buyer right now is not the loudest bidder. It is the one who thinks in shekels, negotiates like the market is soft, protects against currency risk, understands tax status before signing and refuses to confuse a lower sticker price with a cheaper deal.