Japan’s Nikkei Tops 65,000 and the Dow Sits Above 50,000 as Oil Stays Near Crisis Levels — How the World Changed Since 2008

By JBizNews Desk

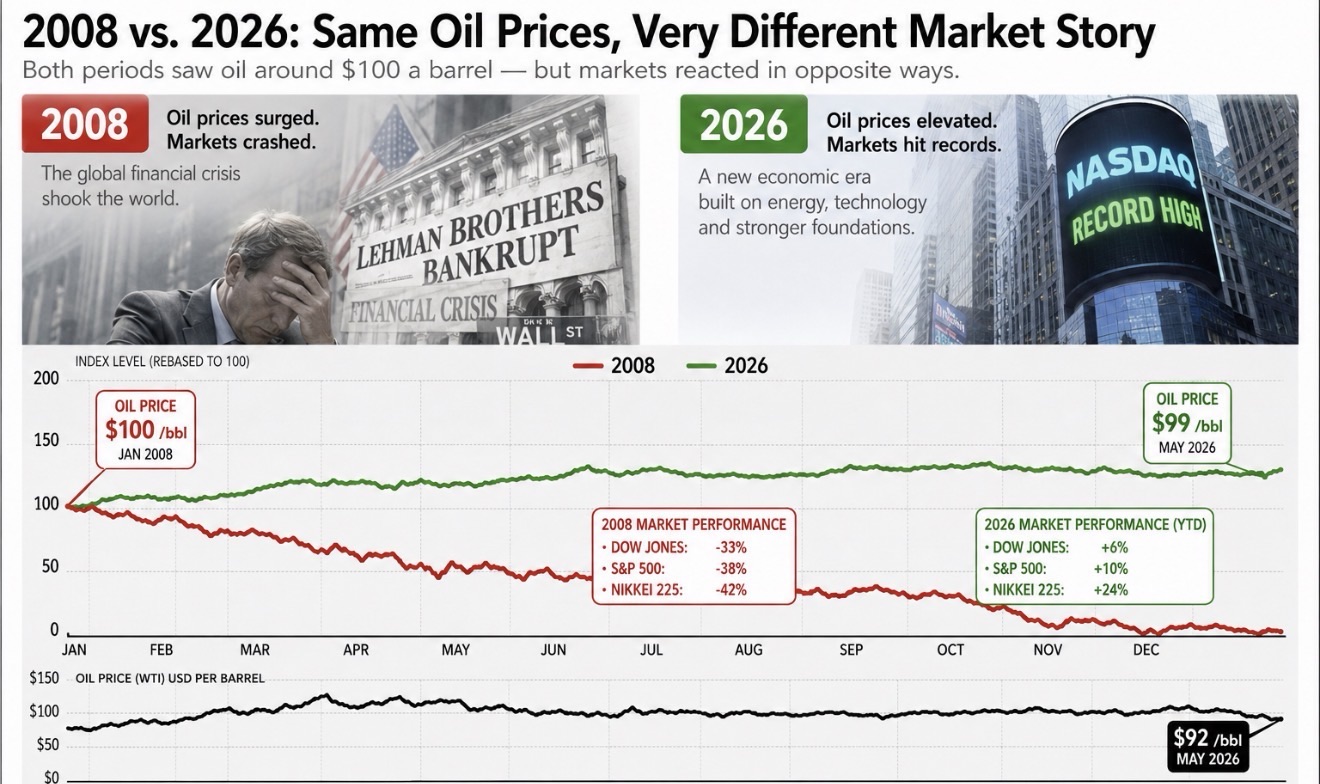

NEW YORK, May 24, 2026 — Japan’s Nikkei 225 crossed 65,000 for the first time in history Monday while the Dow Jones Industrial Average held above 50,000 and oil prices fell sharply on hopes the Strait of Hormuz may reopen soon — a combination that would have sounded almost impossible during the 2008 financial crisis, when soaring oil prices and collapsing financial markets nearly broke the global economy.

The Nikkei surged past the 65,000 mark in early Asia trading as Brent crude fell more than 4% to below $99 a barrel and West Texas Intermediate dropped toward $92 after President Donald Trump said negotiations with Iran were “proceeding in an orderly and constructive manner.” Trump also said he instructed negotiators “not to rush into a deal” because “time is on our side,” while keeping his threat of renewed military strikes against Iran on the table if talks fail.

The Dow sat above 50,000 after Friday’s record close at 50,579.70, while the S&P 500 closed at 7,473.47 and the Nasdaq Composite ended at 26,343.97 — all near historic highs despite a Middle East war that has kept global oil markets under extreme stress for nearly three months.

For most investors and consumers, the obvious question is simple: how?

The world in 2008 looked nothing like the world today. That September, Lehman Brothers collapsed. Bear Stearns had already failed. AIG, Fannie Mae and Freddie Mac were taken over by the U.S. government. Citigroup and Bank of America survived only on federal lifelines. The Dow crashed below 6,600. Oil had touched nearly $147 a barrel that July before collapsing as the global economy froze. Credit markets seized. Home values evaporated. Unemployment doubled. And the consensus view, voiced from Davos to Washington, was that American financial dominance was finished, that emerging markets would lead the next era, and that the U.S. consumer was permanently broken.

If anyone had told a trader in October 2008 — staring at a 6,500 Dow and $147 oil still ringing in their ears — that 18 years later the Dow would be above 50,000, the Nikkei would be at 65,000, oil would be elevated again on a new Middle East war, and markets would be hitting records anyway, that trader would not have believed it. Nobody would have. The world that produced today’s prices had to be built, piece by piece, and most of the construction happened quietly.

The U.S. transformation started with energy. In 2008, the United States was the world’s largest oil importer, sending hundreds of billions of dollars overseas every year to pay for crude. The shale revolution changed that completely. New drilling and fracking technology unlocked the Permian Basin in Texas, the Bakken in North Dakota, the Marcellus in Pennsylvania, and the Eagle Ford in south Texas. By 2018 the U.S. had become the world’s largest oil producer. By 2020 it had become a net energy exporter. Today, when Brent trades at $99, much of that money flows to ExxonMobil, Chevron, ConocoPhillips, Pioneer Natural Resources and hundreds of independent American producers — not to OPEC. In 2008 a $100 oil price drained the U.S. economy. In 2026 it is closer to a wash.

The second transformation was the rebuilding of the banking system. The 2008 crash was not really about oil. It was about leverage. American banks had stacked a pyramid of mortgage-backed securities on top of subprime loans, and when housing turned, the whole credit system collapsed. After the crisis, the Dodd-Frank Act, the Federal Reserve’s annual stress tests, and tighter international capital rules forced banks to hold far more capital and far less risk. Today JPMorgan Chase, Bank of America, Citigroup, Goldman Sachs, Morgan Stanley and Wells Fargo are among the strongest-capitalized banks in the world. Energy shocks now hurt margins. They do not detonate the financial system.

The third transformation was the rise of the technology economy. The companies leading the Dow and the S&P 500 today are not the companies that led them in 2008. General Motors went bankrupt. General Electric was broken up. AIG, Citigroup, Bank of America and Kraft were removed from the Dow or restructured almost beyond recognition. In their place came Apple, Microsoft, Nvidia — added to the Dow in November 2024 — Amazon, added in February 2024, plus Visa, Salesforce, and UnitedHealth. These are software-margin businesses with very little direct exposure to the price of oil. Nvidia, Microsoft, Apple, Alphabet, Amazon, Meta Platforms and Broadcom alone now make up roughly a third of the S&P 500’s market capitalization, and they are growing earnings on a structural AI capital-spending wave that has no real 2008 parallel. Meta has committed to $115 billion to $135 billion in 2026 capital expenditures, almost all of it on AI data centers. That kind of spending becomes someone else’s revenue — and most of it flows straight back into the U.S. corporate sector.

The fourth transformation is the economy underneath all of it. The U.S. economy of 2008 was still heavily industrial. The U.S. economy of 2026 is roughly 80% services. Software, healthcare, financial services, entertainment, professional services — none of them care much about the price of crude. A barrel of oil at $100 is a meaningful input cost for an airline, a chemical company or a trucker. It is a rounding error for a software company billing $50,000 per seat or an asset manager charging fees on $5 trillion in AUM.

Asia’s transformation runs in parallel — and the Nikkei story is the clearest example. For most of the period after 2008, Japan was written off. The country’s stock market spent more than three decades trying to climb back from its 1989 bubble peak of 38,915. It did not break that record until 2024. The consensus view was that Japan was structurally finished — aging population, deflationary economy, frozen corporate culture, government debt over 250% of GDP. The country was a global cautionary tale.

Then the rebuild happened, also quietly. The Tokyo Stock Exchange forced listed companies to improve return on equity, unwind cross-shareholdings, and treat shareholders as actual owners — a corporate governance revolution that took a decade to play out and is still going. Warren Buffett’s Berkshire Hathaway publicly invested in Mitsubishi Corp., Mitsui & Co., Sumitomo Corp., Itochu Corp. and Marubeni Corp., signaling to the world that Japanese trading houses were undervalued cash machines. A weaker yen turbocharged Japanese exporter earnings. And then artificial intelligence arrived — and Japan turned out to own essential pieces of the AI supply chain.

Japanese companies supply the equipment, materials and precision components that make modern AI chips possible. Tokyo Electron, Advantest, Disco Corp., Lasertec, Shin-Etsu Chemical, SUMCO, Fujikura and Furukawa Electric are now essential vendors to Nvidia, TSMC, Samsung Electronics and the broader global semiconductor industry. The Nikkei’s 24% year-to-date gain in 2026 is the world’s strongest among major equity indices and is being driven by the same AI capital expenditure wave lifting U.S. tech — except Japan gets it twice, because falling oil prices also reduce the country’s enormous energy import bill. Nomura Securities senior strategist Takashi Ito put it plainly: “even a modest easing of inflation can provide meaningful relief.”

The Federal Reserve’s position has also changed dramatically since 2008. Back then, the Fed under Ben Bernanke was slashing rates to stop the financial system from collapsing, eventually pushing them to near zero and launching quantitative easing. Today, newly sworn-in Fed Chair Kevin Warsh is holding rates elevated to fight inflation that has stayed above the central bank’s 2% target for years. Markets are climbing despite high interest rates, not because of cheap money — a fundamentally different and arguably healthier dynamic. Fed Governor Christopher Waller said Friday he wants to hold rates steady but would not rule out hikes if energy-driven inflation proves durable. A Hormuz reopening cuts directly against that risk and reopens the path to the rate cuts Warsh has signaled he prefers.

Why are markets rising to new heights in a time like this, instead of crashing? Because the modern economy is built on a different foundation. The U.S. is energy-independent. Banks are over-capitalized. The largest companies sell software, not steel. Earnings are growing on an AI capital expenditure wave measured in hundreds of billions of dollars. Japan has rebuilt itself into a core AI supplier. And the financial system has the shock absorbers it lacked in 2008. The same headlines that crushed the world 18 years ago — Middle East war, $100 oil, central banks under pressure — are now hitting an economy designed to absorb them rather than buckle under them.

None of this means markets are risk-free. Iran’s Supreme Leader Mojtaba Khamenei has ordered enriched uranium reserves to stay inside the country, contradicting Washington’s central demand. Tehran is reportedly working with Oman on a permanent toll system for the Strait of Hormuz, which Trump has rejected outright. The U.S. blockade of Iranian ports remains in place. Goldman Sachs head of oil research Daan Struyven estimates every additional month the strait stays shut adds roughly $10 to the year-end oil price. The math runs in both directions, and the gap between Trump’s threat to strike and his “time is on our side” patience is the gap traders will reprice the moment the next Truth Social post lands.

But the bigger story is the one most investors lived through without quite noticing. The world that made the Dow at 50,000, the Nikkei at 65,000, and oil at $99 impossible in the same sentence has been replaced by a different world entirely. In 2008, nobody would have believed it. In 2026, it is the tape.

— JBizNews Desk

© 2026 JBizNews. All Rights Reserved. Reproduction or distribution without written permission is prohibited.