Credit card and auto loan delinquencies look like 2008. Housing does not

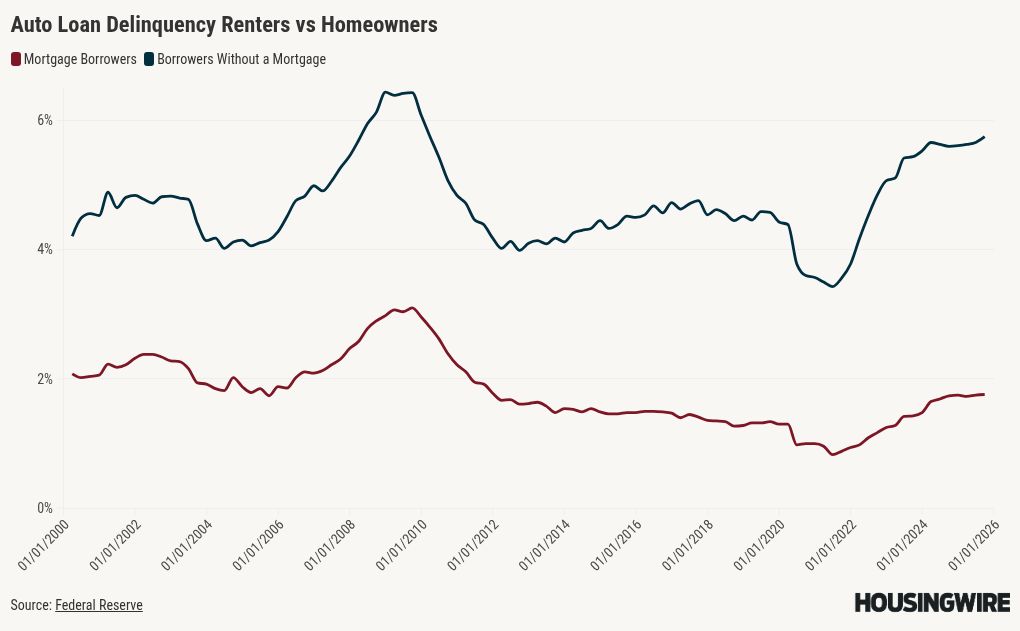

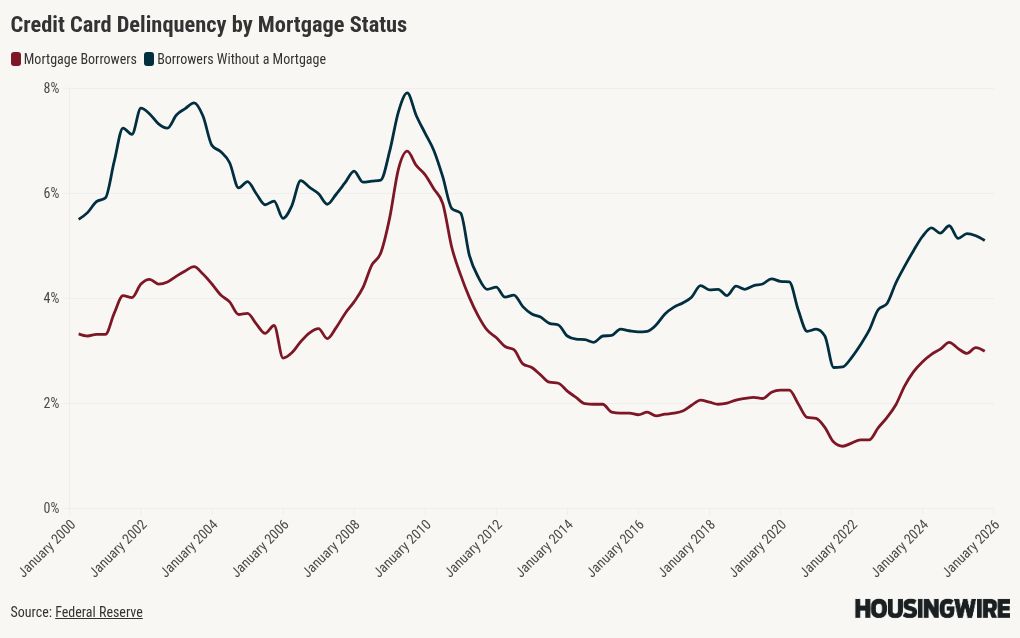

Serious delinquencies (90 days or more past due) for credit cards and auto loans are at peak levels not seen since the Great Financial Crisis, with the savings rate dropping to a low point for 2026.

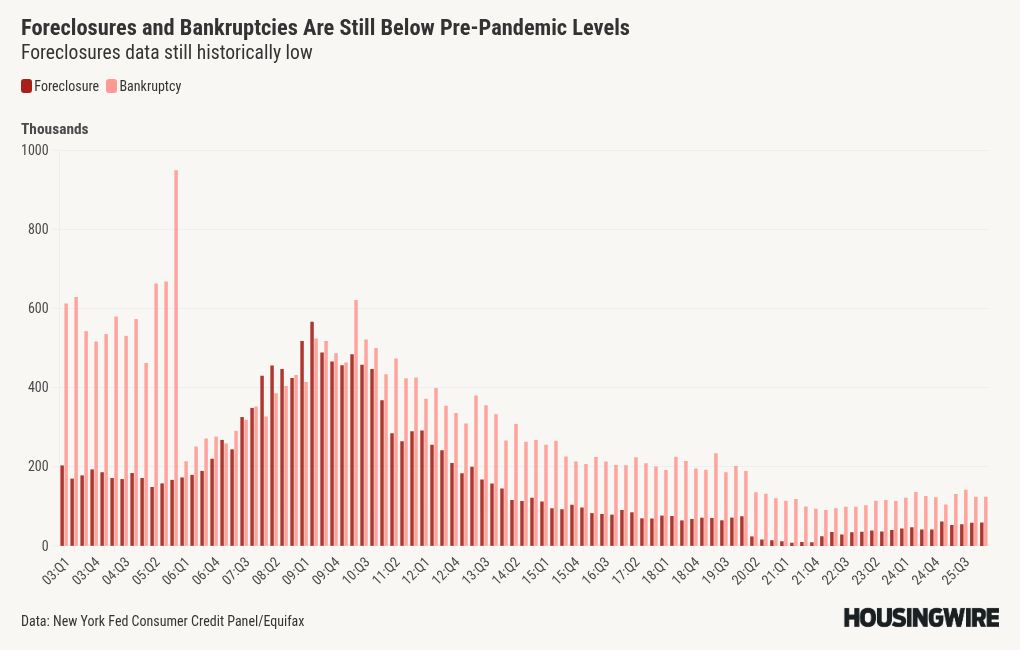

Will this result in a return to 2008 conditions for the housing industry? Many lifelong doomers have showcased the rise in foreclosure data to show we’re on the verge of a similar crash — or something even worse. But the chart below easily shuts down this premise.

I thought I would take a different approach today, since many people are pointing out that credit card and auto loan stress look awful, which is why homeowners are struggling and we could be on the verge of an epic crash. For those who get to see my live events, I always talk about how credit stress for renters is typically worse than for homeowners. Let’s clearly illustrated what I’ve been talking about.

Federal Reserve report on credit stress

One of the questions I often get — which is a valid one — is why the Federal Reserve ignores the financial stress in the auto loan and credit card data. Last year, the Fed wrote this article to give people a view on credit delinquency data.

Again, I believe some people still believe the credit market or the credit data is pointing toward another 2008, a topic that I recently debunked.

At live events, I say that we see stress in renters’ finances more than in homeowners’ financial. In essence, that has always been the case. Below are two examples using credit card and auto loan data. You can see a clear difference between the two groups.

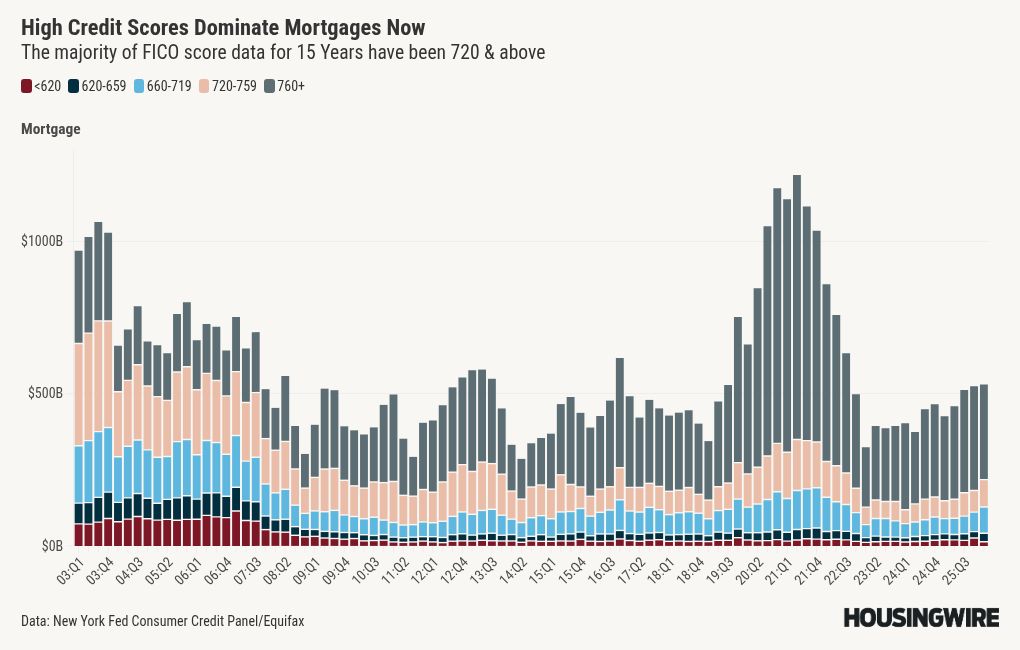

Because of the 2005 bankruptcy reform law and the 2010 Qualified Mortgage regulation, homeowners on paper have never looked better. The FICO score data, cash-flow snapshots tied to making credit and auto loan payments, and scoring on their utilization rates with debt, has never been better in the past 15 years.

A lot of people also point to student loan stress. Well, we have had student loan stress since 2010, and it has never created a surge in housing inventory. This is because most student loan delinquencies are from college dropouts whose loan balances average less than $14,000.

Conclusion

We’ve had many takes on credit card and auto loan delinquencies this week. With the savings rate falling to a yearly low of 2.6% — and with the 12-month average savings rate at 4% — it might make it seem like it’s housing 2008 all over again.

But it’s not: Homeowners are in fine spot and the new listing data since 2013 has never shown seller stress. While the Fed is considering raising rates again, I do believe they need to do a better job of explaining to the public why the credit stress data isn’t a big issue.